Flood damage can be one of the most devastating and costly events an Irish homeowner faces. Understanding how your policy responds before disaster strikes is the difference between a full settlement and an unexpected bill.

Flood damage is one of the most stressful and traumatic types of damage. You will often need immediate alternative accommodation and have to leave your property and all your possessions behind.

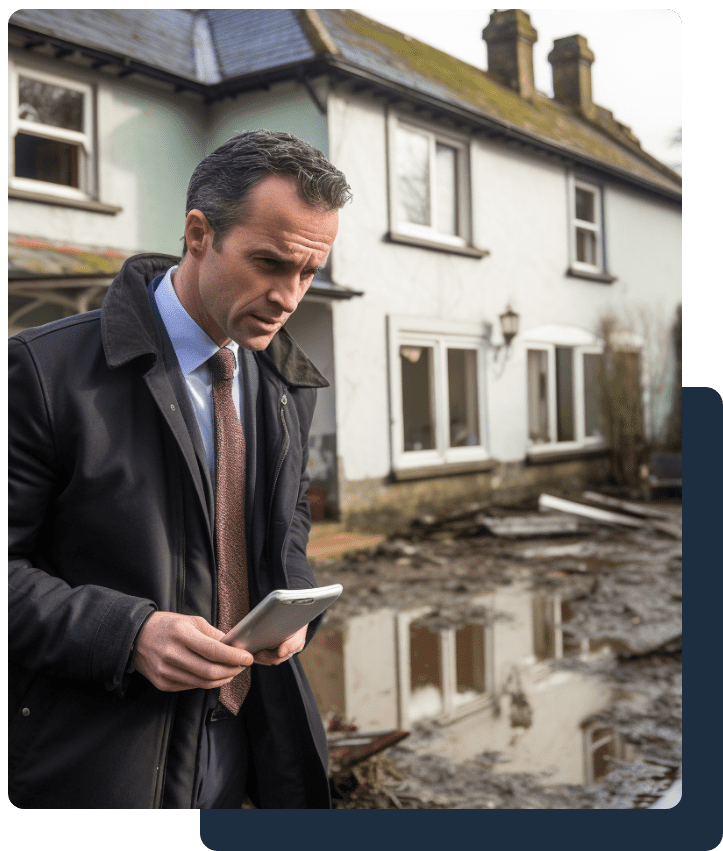

You will be unable to begin assessing the damage and start the drying process until the flood waters subside.

Flood damage claims can be tricky to handle by yourself. The first thing you should do after the incident is to contact Insurance Claim Solutions.

The sooner we visit your home and get a full assessment of the damage carried out, the better the chance of success.

We need to assess quickly what you are entitled to claim for, especially if you think that your policy covers perishables.

With flood insurance claims, the speed of processing of the claim and accurate assessment of secondary damage is very important. It goes without saying that knowing all the rules and regulations, so you don’t invalidate your claim, is also very important.

If you suffered from flood damage, you probably have a lot of questions:

What do I do first?

What am I covered for?

Will the flooding cause rot to my building?

Does it need to be treated?

Do I need specialist cleaning contractors?

Where do I find the contractors that specialise in flood damage restoration?

How long will it take to dry?

Does the area require sanitisation?

If you have flood insurance and recently experienced flooding, you will need to submit a flood damage claim before you can start the repairing process. Insurance Claim Solutions will help you through all the steps of the claim process.

We will help you assess the damage, prepare the claim, deal with the insurers and negotiate your settlement so you can get your life back to normal as soon as possible. We have a very high success rate, have a look at our testimonials.

Flood damage claims are among the most complex insurance claims to navigate successfully. Unlike other types of property damage, flood damage often involves multiple layers of destruction that extend far beyond what’s immediately visible. Water damage can penetrate deep into building structures, creating long-term problems that may not surface for weeks or months after the initial flooding event.

When dealing with flood damage to your property, the immediate water damage is often just the beginning of your concerns. Flood water can cause extensive structural damage to foundations, walls, flooring, and electrical systems. Additionally, the moisture left behind creates ideal conditions for mold growth, wood rot, and corrosion of metal components throughout your home or business premises.

Understanding what constitutes flood damage under your home insurance policy is crucial for maximising your insurance claim payout. Many policyholders are surprised to learn that their standard home insurance may not cover all types of flooding, making it essential to work with an experienced public loss assessor who understands the intricacies of flood insurance coverage.

Our insurance loss assessor team helps identify and document various categories of flood damage that many property owners overlook:

Direct Water Damage: This includes immediate damage caused by flood water entering your property, affecting floors, walls, ceilings, and personal belongings. Our loss assessors conduct thorough water damage assessment to document all areas impacted by flooding.

Structural Damage: Flood water can compromise the structural integrity of your building, affecting foundations, load-bearing walls, and support systems. This type of damage requires expert assessment to identify both immediate and potential long-term issues.

Electrical System Damage: Water and electricity don’t mix, and flood damage often results in complete electrical system replacement. Our damage assessment includes comprehensive evaluation of all electrical components that may have been compromised.

Don’t let the stress of dealing with insurers and repair contractors overwhelm you. Contact us today, and let us handle your insurance claim while you focus on your recovery.

WhatsApp us